Handling claims “well” must be a core value of any insurance carrier or they are negating their responsibility and duty to their customer.

In the context of a claim under a personal lines insurance policy, the word “adjust” generally means to determine the value of the loss/damage to be paid to the policyholder/insured, as prescribed by the insurance policy. In sum, claims are basically demands against an insurance policy by the policyholder/insured and adjusting is the process wherein the claim value is determined and, if covered, paid. In the simplest of terms, the adjusting of a claim is the fulfillment of the contract between an insurance carrier and the policyholder/insured.

Even though, most everyone has auto insurance because it is mandated by the State, people also want to protect their investment, and they want to protect their assets against any liability they may incur from driving a vehicle. So, once a claim occurs, the insurance carrier has the obligation to fulfill that promise to their customer to protect them and make them whole again. Handling claims “well” must be a core value of any insurance carrier or they are negating their responsibility and duty to their customer.

In the J.D. Power 2018 U.S. Auto Claims Satisfaction Study SM the industry hit its highest level of satisfaction since inception of the study, at 861.1 Even though the industry continues to improve, of the 24 top profiled carriers in the study, 14 of the carriers fell below the industry average. Not being the highest rated carrier in the 2018 U.S. Auto Claims Satisfaction Study doesn’t mean the carriers are not fulfilling their duties to their policyholders, but it does point out that there is still room for improvement in the handling of claims by the industry.

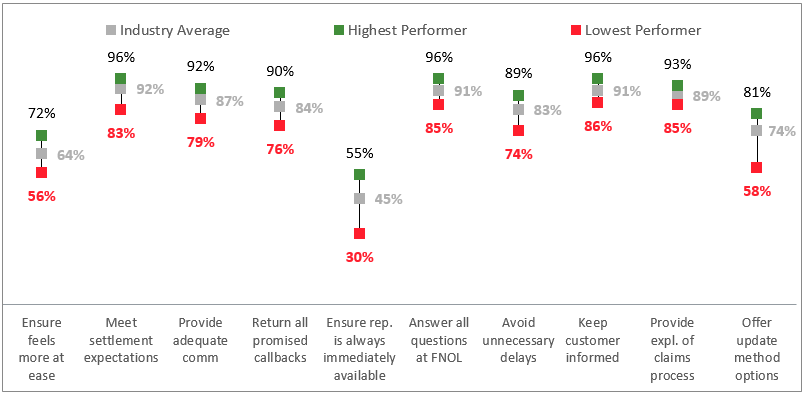

What the Auto Claims Satisfaction Study found was a continued need for improvements in making customers feel more at ease, being available, and providing better communication options. Of the top KPI’s, ease, availability, and options were the bottom three and had wide swings between the top and bottom performers.

Top 10 KPIs: Range of Performance

Availability continues to be the lowest rated KPI and much of that availability is due to carriers not offering update methods that match the customer’s preferences or not staying ahead of the customer with status updates and not providing active updates that don’t require the customer to take some action to find out the status of their claim. When a customer needs to call their carrier for some reason, the customer reports the carrier availability at 38%. This need again is generally created because the customer doesn’t know what is happening with their claim. Providing a more proactive claim process update to customers could not only improve the availability issues but also reduce the number of inbound calls to the carrier freeing up the staff to focus on adjusting claims. Finding a better solution to this issue is a win-win for the carrier and customers.

Creating a digital pathway from the carrier to the customer that is timely and informative is likely the key to availability going forward. In the Auto Claims Study, we found customers preference for using text is still low at 18% but that preference is growing, and when text is used the overall customer satisfaction is 883, again on a 1,000-point scale. The use of an informative text message, one that does not require the customer to take any further action, has the highest overall satisfaction score of any communications method measured by 10 points over the next highest method. It is 25 points higher than the most preferred method of communication which is calls from the insurer. Creating a proactive and preferred communication method not only improves availability but it also addresses the update methods KPI and will help to make the customer feel more at ease.

Customers reported that keeping them better informed on what to do next boosted their sense of ease and, from that, improved overall satisfaction. Additionally, 20% of the survey responses felt that if the carrier provided services and information more quickly that too boosted their sense of ease. Addressing this issue is another area where a digital solution can create a greater sense of speed in the adjudication of the claim which supports an easing of tensions on the part of the customer.

All in all, claim organizations have spent a great amount time and money building highly effective automation to streamline the claim process but much of the efficiency built into the system is not customer facing and does not provide the customer with a greater sense of ease. It doesn’t improve the feeling that the carrier is empathetic to the customer claim; it doesn’t reduce the need to follow-up; and in many cases it puts the onuses on the customer to put more effort into resolving the claim than the customer feels is necessary. Given that the personal auto market is stagnate and the only real product a carrier is selling is their ability to handle claims, it might be in the best interest of every carrier not in the top rankings of the J.D. Power 2018 U.S. Auto Claims Satisfaction Study to understand what it might take to reach that level and further to reevaluate their commitment to the customer because customers are not going to accept a lower standard of performance from any vendor regardless of price much longer.

1The ranking is based on a 1,000-point scale.