It isn’t often you need to give blood or fill out a health assessment before buying a product, but many individual life insurance policies require just that. Soon after these activities are done, however, the policyholder is sent on their way with their brand-new life insurance policy and not much direction or expectation of follow-up. They may only occasionally think about their policy, usually when their premium comes due.

The customer experience is often overlooked in the life insurance industry as life insurance products are typically low touch, outside of the sales experience which, as noted above, may be higher touch than purchasing other types of products. Life insurers who do invest in customer experience, however, are poised to reap the rewards of higher engagement and more satisfied customers, which in turn can lead to higher product consideration and brand advocacy.

With this in mind, let's examine the 5 mega trends influencing the future of life insurance and how we can expect customer-centric carriers to respond in the coming years.

- Focus on data-driven underwriting and risk assessment

- Growth of direct-to-consumer life insurance sales

- Increased focus on financial wellness and holistic financial planning

- Personalization of life insurance products, services, and communications

- Digital transformation and enhanced customer engagement

Focus on Data-Driven Underwriting and Risk Assessment

Insurers will increasingly leverage advanced analytics to assess risk and price policies more accurately. Innovative technologies such as accelerated underwriting and predictive analytics, can make it easier for individuals to obtain life insurance coverage quickly and with less stringent requirements, ultimately streamlining underwriting processes. However, the concern for cybersecurity and the need for data protection will become an even greater concern. Customer-centric insurers will look to invest in robust security measures to protect customer data, and ensure they are communicating these efforts to customers so they feel that their data is in the right hands.

Growth of Direct-to-Consumer Life Insurance Sales

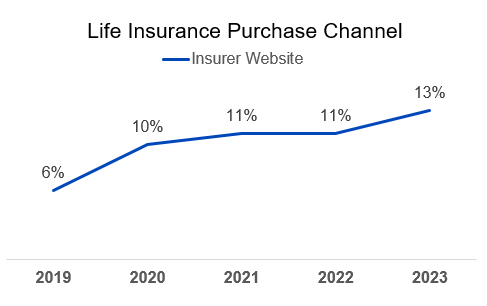

Consumers are increasingly comfortable buying life insurance online, especially term policies. The J.D. Power U.S. Individual Life Insurance Study revealed that in 2019 only 6% of survey respondents bought their individual life policy on an insurer’s website. By 2023, however, that figure more than doubled to 13% and satisfaction is 45 points higher for those who purchased their policy on the website vs. those who didn’t.

Insurers who offer the option to purchase life policies online will likely continue to grow market share, which will put pressure on life insurers to improve their digital sales experience. Watch for customer-centric brands to continuously enhance and streamline their digital sales channels as customer expectations and digital tools evolve.

Increased Focus on Financial Wellness and Holistic Financial Planning

Many life insurance providers recognize that they can play a more significant role in their customers' overall financial well-being, and customers are following suit. J.D. Power data shows that individual life insurance customers are purchasing their life insurance to fulfill financial planning purposes (asset accumulation, vehicle funding, retirement income protection, long-term care funding, tax planning) vs. only purchasing a policy to cover final planning purposes (pay for final expenses, allow my family to maintain standard of living, leave money to dependents, leave money to charity) at higher rates in 2023 (51%) than in 2019 (36%). This is especially true for permanent policies, with 62% of customers purchasing for financial planning purchases.

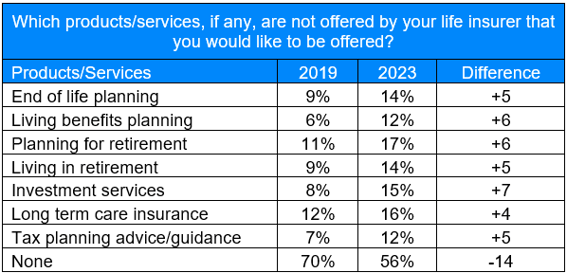

Customers are receptive to life insurers continuing to expand their service offerings, such as financial planning tools and educational resources. The exhibit below shows the products/services customers are interested in their life insurer providing to them in 2019 vs. 2023. Interest in each product/service type asked about has increased during this time, with investment services having the largest increase in interest. Younger customers (Gen Z and Millennials) are the most interested in having their life insurance company offer more services to them, while interest dwindles as customers age, likely because they already are receiving these services elsewhere.

Customer-centric carriers will continue to examine opportunities to expand their offerings and will focus on communicating these offerings throughout sales, onboarding, and servicing cycles.

Personalization of Life Insurance Products, Services and Communications

As life insurers look to offer a more comprehensive suite of services, there will be an increased focus on offering customizable life insurance products that can be tailored to meet the specific needs of individual customers.

We are already seeing this trend with accelerated underwriting for term policies, which allows customers to get life insurance with no medical exam. These policies are more expensive and may have lower death benefit limits but fill a need for many consumers who have health conditions that may disqualify them from receiving medically underwritten life insurance. These policies are also quick and low effort on the part of the life insurance applicant, making it a favorable option for someone who doesn’t have the time to go through the application process of a medically underwritten policy and doesn’t require a large payout.

Customer-centric insurers are likely to leverage data and analytics more extensively to better understand customer behaviors and preferences. This can lead to personalized insurance offerings, individualized services, and more accurate risk assessments, enhancing the relevance and attractiveness of life insurance products. And this enhanced focus on individual customer needs has the potential to significantly impact the customer experience. Customers who feel that their last contact from their life insurance company was tailored to their individual needs have an overall satisfaction 146-points higher than those who didn’t feel that the contact was tailored to their needs. These customers are also much more likely to purchase another product from their insurer – 50% of those with tailored communication state they definitely will purchase another product vs. only 28% of those without a tailored communication.

Digital Transformation and Enhanced Customer Engagement

Digital engagement has grown significantly over the past 5 years. When we look at customers who have interacted with their life insurer within the previous year, only 30% had a digital (email, website, chat, app) interaction in 2019, but by 2023 that number increased to 49%. And this increased digital engagement is benefiting end users. Individual life insurance customers who have interacted with their carriers through digital channels are significantly more likely to understand their life policy and what it covers and be more satisfied with their life insurance experience overall.

In response to this, customer-centric carriers will continue to shift towards digitalization adopting online platforms for policy sales, underwriting processes, and customer service and investing in technologies that facilitate ongoing communication, education, and support for policyholders. For example, digital document submission, such as electronic signatures, will continue to grow in 2024, simplifying and expediting the application process, and increased focus is expected to be placed on mobile apps and interactive tools that can enhance the overall customer experience.

We can’t ignore the potential impact of artificial intelligence (AI) and automation on every aspect of the experience from the underwriting processes to claims management to customer service. AI-powered chatbots will become more sophisticated, handling complex customer inquiries and streamlining the application process. This can expedite decision-making, reduce operational costs, and enhance overall service efficiency.

Bonus Trends to Watch

Although the 5 mega trends listed above are likely to have biggest impact on the consumer experience with individual life insurance carriers and products, here are some other “bonus” trends we are watching closely that could impact the industry:

- Increased focus on ESG (Environmental, Social, Governance): ESG investing was all the rage back at the height of the COVID-19 pandemic and has continued to gain traction; although, maybe not to the extent that many hoped it would. Life insurers may incorporate ESG factors into their permanent life insurance product offerings, creating sustainable or socially responsible life insurance products that align with customers' values, possibly attracting younger consumers to their book of business.

- Advanced Insurtech ecosystems: Insurance companies might collaborate with wellness providers, wearable tech companies, and even employers to create comprehensive health and financial ecosystems. This could incentivize healthy habits and provide more holistic protection. The development of these ecosystems could also lead to the growth of embedded life insurance products. The seamless integration of life insurance into other financial products or services, like offering a small term life insurance policy through a mobile banking app, could make life insurance accessible to more people, especially those in underserved markets.

- Gamification and incentives: More collaboration and better integration could lead to the use of gamification techniques to encourage healthy behaviors and engagement with life insurance policies. Some insurance companies have already implemented these types of incentives, but this trend could expand across more carriers and policy types.

- Focus on underserved markets: Innovative product design and streamlined application processes could help make life insurance more accessible and affordable for underserved markets, such as gig workers, those with pre-existing conditions, people with lower income or who live in rural areas, and some racial and ethnic groups.

Wrap Up

The 5 mega trends (and 4 bonus trends) outlined above will be influenced by various factors, including technological advancements, regulatory changes, and consumer preferences, but continued, focused improvement on the customer experience can strengthen customers’ relationships with their life insurance carrier. These stronger relationships can be leveraged to increase products consideration and brand advocacy. Through thorough examination of Voice of the Customer data, we will continue to monitor how these trends impact the customer experience for individual life insurance policy holders and reveal how brands are meeting and exceeding customer expectations.

To discuss the trends outlined in this article further and to discuss the latest life insurance customer research and analytics, contact our team today.

About the Author: Breanne Armstrong is Director of Insurance Intelligence at J.D. Power. Her area of focus is on the customer experience in auto, property, and individual life insurance and annuities. She has over 15 years of research and consulting experience and 7 combined years at J.D. Power working within the Insurance Practice.

Where to find more insights like this:

This blog post was featured in the Insurance Insights monthly newsletter. Make sure you're signed up to get the latest insurance intelligence >

Share this

5 Mega Trends Influencing the Future of Annuities

Can UBI Turn Shoppers into Advocates?

No Comments Yet

Let us know what you think