Usage-Based Insurance (UBI) programs are becoming more influential to customers throughout their relationship with their insurer. As we seek to better understand the influence, let’s first look at the impact of UBI on shopping decisions.

Make or Break the Bundle

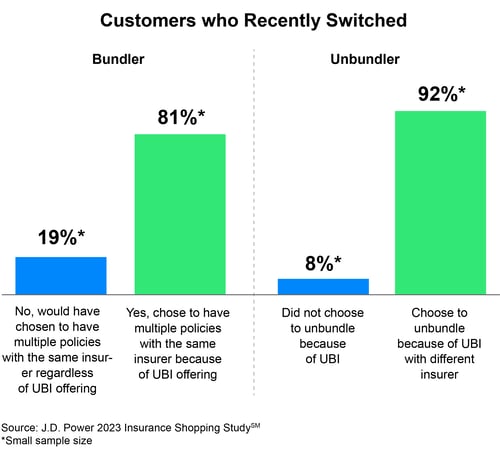

A recent survey revealed the large influence UBI programs have on buyer behavior. Rising insurance rates have customers seeking ways to save on their auto insurance premiums, and many are turning to a UBI program to help lower costs. Shoppers who switch carriers indicate UBI is taken into consideration in their decision to bundle or unbundle.

Of those who bundle after recently switching, 81%* say they choose to have multiple policies with the same insurer because of a UBI offering. For the unbundlers who switch, 92%* attribute their decision to unbundle to of a UBI program offered by a different insurer.

Unbundlers prioritize savings with 70%* choosing different insurers for auto and home coverage in order to save money on premiums.

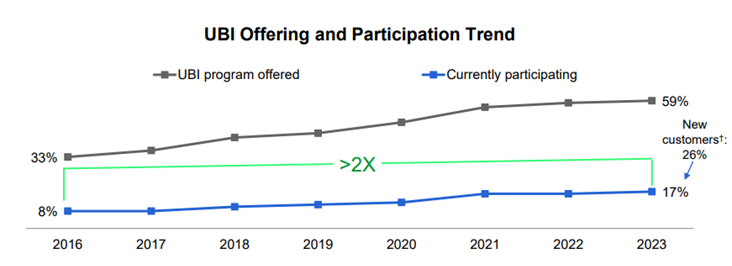

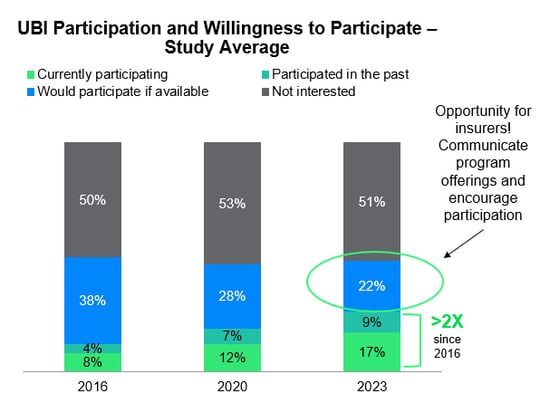

New Customers Drive Participation

The attractiveness of UBI programs for cost savings is paying off as participation in these programs has more than doubled since 2016. New customers especially appear to find value in these programs with 26% indicating they participate in UBI programs compared with 17% overall.

Source: J.D. Power 2023 U.S. Auto Insurance StudySM

†New customers are defined as less than 1 year tenure with their current insurer.

The Risk

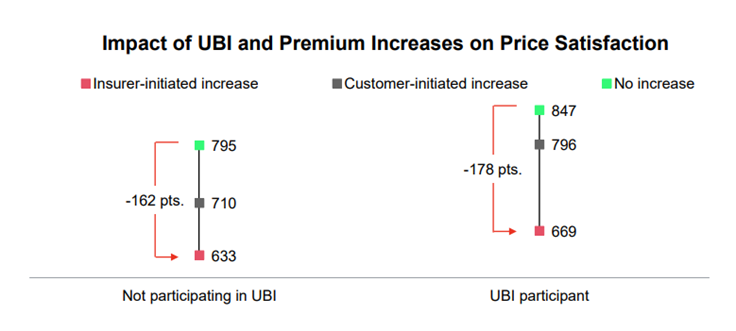

Given the cost-saving appeal of UBI programs, it should come as no surprise that participants are upset by an insurer-initiated premium increase. While UBI participants are more satisfied overall with price than non-participants, the impact of an insurer-initiated increase is greater on UBI participants (178 points lower than those with no increase vs. 162 points lower for non-participants).

Source: J.D. Power 2023 U.S. Auto Insurance StudySM

The Reward

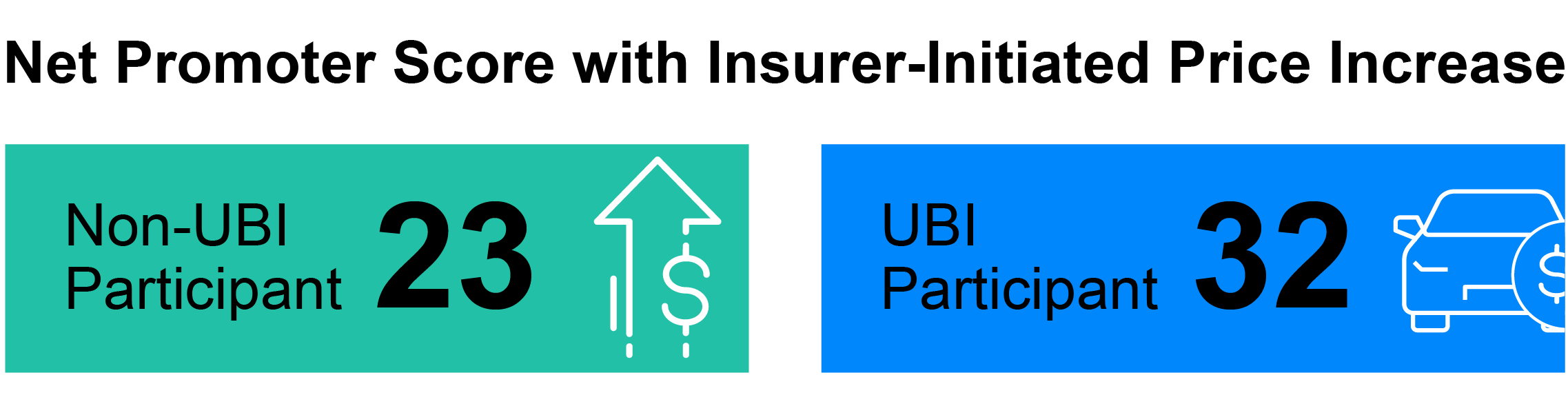

While price increases have a stronger impact on UBI participants than non-participants, this isn’t enough to overcome the stronger advocacy that these customers exhibit. UBI participants are significantly more likely than nonparticipants to say they “definitely will” recommend and renew with their insurer. Even with a price increase, UBI participants have a Net Promoter Score (NPS) of 32 vs. 23 for non-UBI participants with a price increase.

Source: J.D. Power 2023 U.S. Auto Insurance StudySM

Source: J.D. Power 2023 U.S. Auto Insurance StudySM

In addition to retention and advocacy influence, UBI participants also have significantly more favorable perceptions of their insurer’s affordability, trustworthiness, convenience, and reputation, with the largest positive gap in ratings of being innovative.

The Opportunity

In addition to those already engaged in a UBI program, 22% of customers indicate they would participate in such a program if it were available. Considering the positive influence UBI programs have on both purchase decisions and brand advocacy, brands that have these programs already available should ensure that shoppers are aware of this offering and take steps to communicate the value to existing customers. Insurers not yet offering such a program should consider the value to the customer and their brand as reasons to make such a program available.

Source: J.D. Power 2023 U.S. Auto Insurance StudySM

Source: J.D. Power 2023 U.S. Auto Insurance StudySM

For more UBI program insights, including factor performance, influences on UBI satisfaction, and the impact of UBI savings, contact the team or reach out to your account representative today to discuss the UBI segment results recently published as part of the 2023 U.S. Auto Insurance Study.

Share this

Insurance Shopping One Year Later

The Impact of Inflation on Insurance Shopping

No Comments Yet

Let us know what you think