If you were to rent a car, you would expect that a more expensive vehicle would cost more to rent. You would also expect that if you damaged that more expensive vehicle, it may cost more to repair. So, you would not be surprised to see a higher cost insurance option associated with the more expensive (and perhaps more powerful and/or luxurious) versions offered in a series of vehicle options.

While that line of thinking is intuitive, your regular insurance program for your vehicle is not working quite like that – at least not yet.

While the base price of any vehicle can move your insurance rate north, as you add on optional equipment to that vehicle, most current insurance pricing systems don’t take those new features into account. Existing pricing models ignore anything beyond the base price new from an MSRP on the window sticker. What might be more surprising, that is the last time they think about the value of your car– traditionally, it’s all downhill from there.

Why is this the case? Let’s take a step back in time.

The very first auto insurance policy is attributed to Travelers insurance in 1897 for a risk in Ohio. Other auto insurance companies, like State Farm and USAA, recently celebrated 100-year anniversaries for insuring consumer vehicles. While it’s exciting to see brands across the industry celebrate such a marker, we also just weeks ago saw the very first loss in an annual report in 100 years for one insurance company – something we think can largely be attributed to missing the changing conditions on the value of a used vehicle.

Over the last century of auto insurance, paper policies managed in mailboxes and inbox bins have been increasingly replaced by digital policies on smartphone apps in the cloud, however many legacy processes have not kept up with the times. Two iconic pieces of automotive and auto insurance history come to mind – the use of base price new MSRP to set a value in a “set it and forget it” fashion and the use of a one-size-fits-all factor curve for setting a relativity-based insurance value for a vehicle over time (across the nation or within a state).

Why should these processes be left in the past?

We will save the window sticker story of base price versus total price and the gap between the two for another day. Today, we want to spend a moment exploring active valuation methods versus static and embedded methods of predictive models for valuation when it comes to insurance to value for vehicles. Model risk management disciplinarians may not have gotten around to vehicle valuation for pricing yet – the use of base price new and no further detailed tracking of the asset is deep in tradition and only noticeable in filings and rating algorithms, so hidden in plain sight. The current displacement in valuation trends, however, has completely uncoupled the traditional approach from today’s reality.

Let's explore this further.

Model Risk Matters - Active vs. Static Methods

One of the more longstanding traditional presumptions since the time before computers were introduced and data was manipulated with slide rules and look up tables, is that vehicles always get cheaper with age – not a shocking thought, but in recent volatile car valuation times, this embedded thinking has turned into a systemic risk (model risk). Let’s look at a specific case and then the general case.

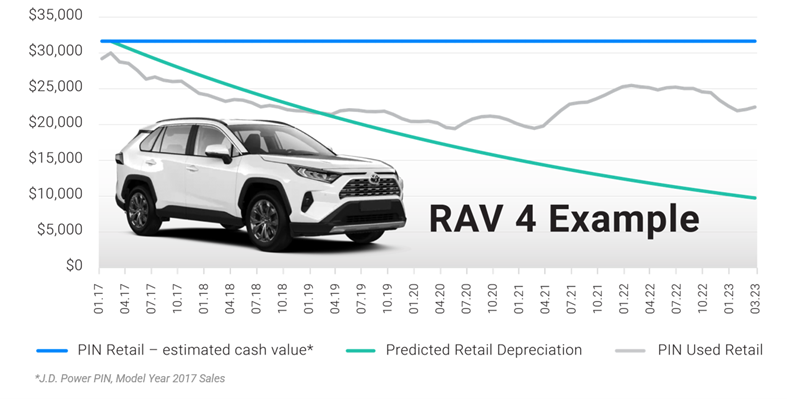

The Toyota 2017 Rav4 model year value trend:

A specific example in these pandemic era times

Prior to April 2020, the market for a used 2017 Rav4 followed a traditional rule of thumb straight line depreciation of about 20% a year – meaning in 5 years it would have lost 2/3 of its original price - $30k-ish moves to $10k-ish across 60 months (see the green line in the Rav4 exhibit).

While other things that consumers insure, like houses, rings, art, etc., all seem to cost more over time – sometimes intrinsically and sometimes due to inflation – the cost for cars normally is presumed to trend downward as they wear out their mechanical function with usage. Nowadays, however, are not normal.

In recent years, scarcity of vehicles and other issues have resulted in a surge in used car values – sometimes going above their price new, often holding value instead of plunging, and generally not depreciating as in “normal” times (see the gray line in the Rav4 exhibit). Values can also vary from type of vehicle to brand of vehicle and perhaps to the trim level and optional equipment for popular configurations – not a one-size-fits-all situation.

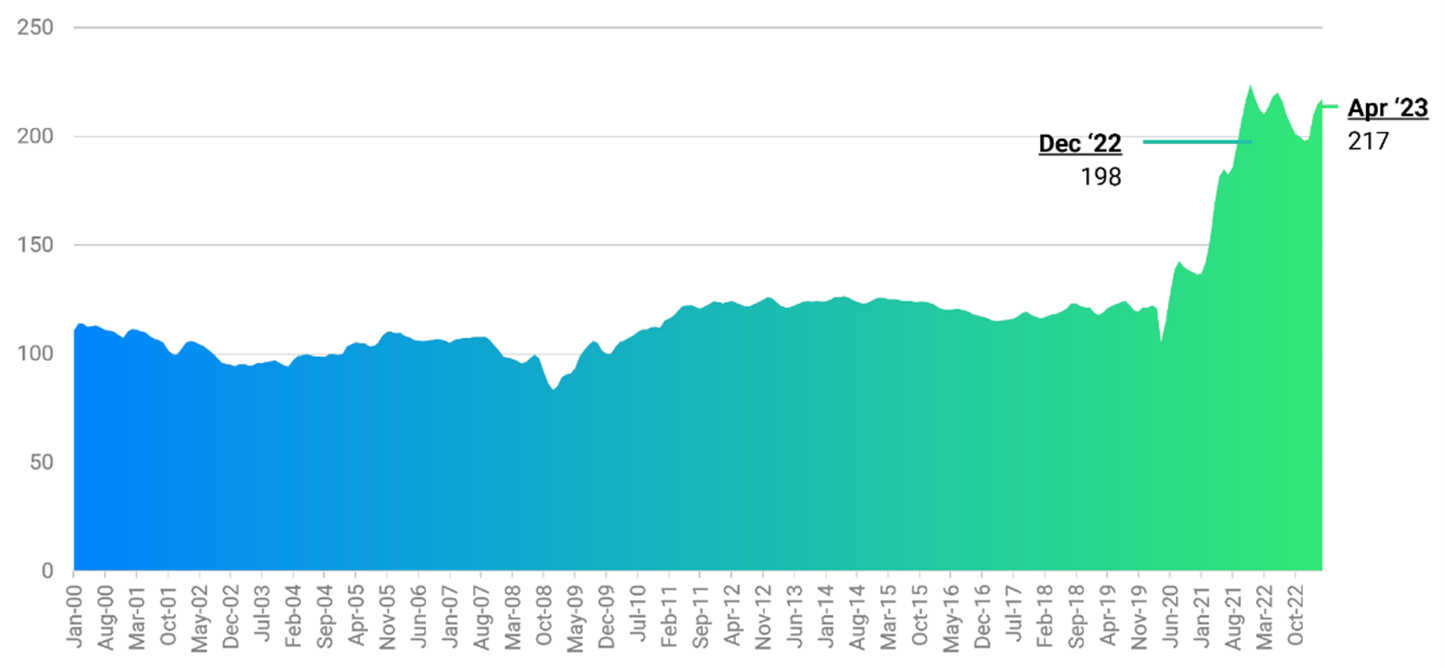

The J. D. Power Used Vehicle Price Index (UVPI), constructed to measure relative market valuation for vehicles below eight years old (a classic plan for targeting under 100,000 miles on the odometer), indicates that since the turn of the millennium in the year 2000 until the beginning of the pandemic in 2020, there were relatively “calm seas” in the used car price space.

J.D. Power Used Vehicle Price Index:

Trend from January 2000 - April 2023

We observe a notable down swell during the global financial meltdown in late 2008 (and follow on recession), with a new plateau in pricing slightly higher for post-recession than pre-recession. There were many insurance pricing increases put into effect to adjust to that new plateau of value of vehicles about a decade ago, but otherwise, we see a relatively uneventful twenty years of valuation on an indexed basis.

That is until the pandemic.

What we see today indicates that a sea change like never before has hit the shore of used vehicle values. Every pricing system, every actuarial triangle, and any predictive model using the last 20 years or more of historical data are ignorant of this kind of volatility and unprepared to say what should happen next.

It's time for insurers to change the way they look at vehicle values.

Today, it seems every auto insurance company is raising rates across the board on a more frequent basis and at higher amounts than any time in our lives. Even with the current rate rising tide, however, we have not seen enough increase to match the change in the most valuable parts of the parc which are up almost double (from the 1-teens to the 2-teens) in the most recent months of the UVPI.

While it is impossible to know what will happen next, it seems the insurance industry can comfortably assume they need to really pay attention to the value of vehicles they insure in a different way than they have so far in order to be around for the next 100 years.

About the Author: Marty Ellingsworth is a leader in creating value from data and digital assets with advanced analytics. He is a strong advocate for customer centricity and has created innovation within and between almost every link in the P&C insurance value chain in both commercial and personal lines.

We’re just scratching the surface on the breadth of better vehicle data that is now available to insurers to inform and improve their pricing and valuation strategies. If you’d like to discuss vehicle valuation data more in-depth, let’s connect.

Where to find more insights like this:

This blog post was featured in the P&C Insights monthly newsletter. Sign up for future editions and explore what you might have missed.

Share this

Know What You’re Insuring: Putting It All Together

Mercedes-Benz Takes Legal Responsibility for Its Level 3 Technology

No Comments Yet

Let us know what you think